But the situation is reminiscent of last August. All signals before that meeting were for policy to stay unchanged, not least because inflation was higher than it had been in 2010, the last time the Fed acted, and it was rising rather than falling.

In the last ten days leading up to that August FOMC, however, came the debt ceiling debacle, an S&P downgrade of US debt, and full scale market panic about growth. In the end, that meeting produced the Fed’s forecast of low rates “at least through mid-2013”. The next Fed meeting will conclude on 20th June, three days after Greece holds fresh elections, and the potential for similar market turmoil is considerable.

Eurozone Checklist:

-Merkel backs away from pure austerity to a balance of austerity and pro-growth policies.

-Germany accepts higher wage/consumer inflation so as to increase the relative competitiveness of weak peripherals.

-Euro bonds are approved by a means of joint Euro zone financing, including joint liability of Euro zone countries.

-The EFSF/ESM provide funds directly for bank recapitalizations.

-ESM is granted a bank charter and gets unlimited access to ECB liquidity.

-A U.S.-like FDIC program is introduced for Euro zone bank deposits.

-The ECB cuts its target rate by 25 to 50 basis points in June or July and reintroduces the Security Markets Program.

-Greek elections on June 17 bring a pro Troika coalition.

-Labor reform begins.

-There is increased fiscal integration including heightened monitoring of eurozone deficits, spending, and movement toward tax harmonization.

Az első már megvalósult, várjuk a többit.

Ha lemegy a para a görögökkel és a spanyolokkal, itt az indok a következőre.

CDS forgalom: a francia második hely és a német ötödik mindenképpen némileg meglepő.

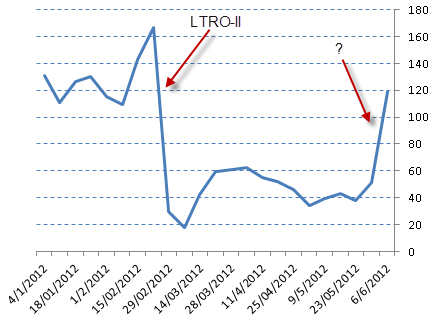

Az európai központi bank rövid lejáratú hitele az utóbbi időben szépen csendben megduplázódott. A pletyka szerint a csütörtöki spanyol kötvénykibocsátás volt belőle finanszírozva.

Update: a nagy parában az olasz kötvény sem mozdult, valószínűleg az ott benne volt az ECB keze

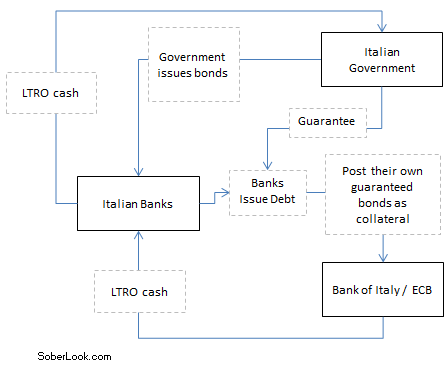

Ennek a mechanizmusa a következő ábrán látható:

1. Banks would issue bonds and retain them (a bank would effectively lend to itself).

2. The government would slap a guarantee on those bonds (after all it doesn't directly cost the government anything for this guarantee).

3. The banks would then post their own bonds with the ECB, who accepted them as collateral because of the government guarantee. Using these bonds as collateral the banks would borrow under the LTRO program.

4. With this new LTRO cash the banks would buy Italian government paper, which they also posted as collateral to borrow more or would hold the paper in reserve to meet margin calls.

-----------

QE3 remény: nagy fehér gyertya 5 napja, majd Bernanke nem erősítette meg: nagy piros gyertya tegnap. Most az arany piac úgy néz ki, hogy: pénznyomda, akkor fel, ha nincs nyomda, akkor le.

Ajánlott bejegyzések:

A bejegyzés trackback címe:

Kommentek:

A hozzászólások a vonatkozó jogszabályok értelmében felhasználói tartalomnak minősülnek, értük a szolgáltatás technikai üzemeltetője semmilyen felelősséget nem vállal, azokat nem ellenőrzi. Kifogás esetén forduljon a blog szerkesztőjéhez. Részletek a Felhasználási feltételekben és az adatvédelmi tájékoztatóban.